11th Edition of the Steady Gains Newsletter

Justin D. Caldwell - Jul 15, 2026

This month, Tanya successfully completed the Conduct and Practices Handbook course. Together with her Canadian Securities Course credential, this strengthens her knowledge of Canadian securities regulation, compliance standards, and professional cond

Investing in Our Team

This month, Tanya successfully completed the Conduct and Practices Handbook course. Together with her Canadian Securities Course credential, this strengthens her knowledge of Canadian securities regulation, compliance standards, and professional conduct.

For our practice, this adds further depth to the support behind account administration, trade execution, and the high standard of care we bring to managing your financial affairs.

Please join us in congratulating Tanya on this important achievement.

From Dividends to a Portfolio Paycheque

For many investors, dividends feel different from the rest of a portfolio’s return. They arrive as cash, are easy to see, and can create the impression that income has been earned without touching the original investment.

That distinction is less meaningful than it appears.

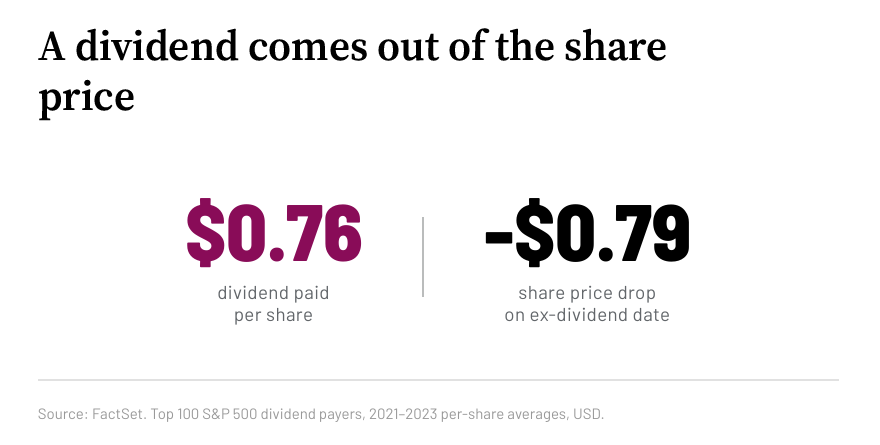

A dividend is part of your return

When a company pays a dividend, cash leaves the business and is transferred to shareholders. The share price typically falls by roughly the amount paid.

This does not make dividends undesirable. It simply means they are one component of total return, alongside interest and capital appreciation.

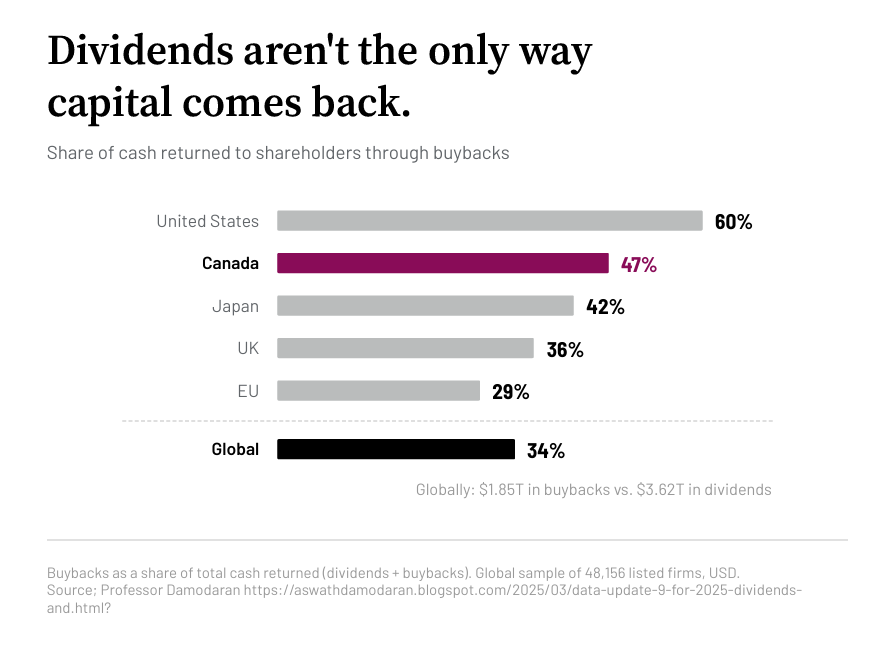

Focusing too heavily on dividends can also narrow a portfolio. Many companies reinvest profits, repurchase shares, or do not pay dividends at all. In Canada, a dividend-focused approach can create greater exposure to a small number of sectors, including banks, pipelines, and utilities.

Our goal is not to produce the highest possible yield. It is to build a diversified portfolio capable of supporting your spending needs through multiple sources of return.

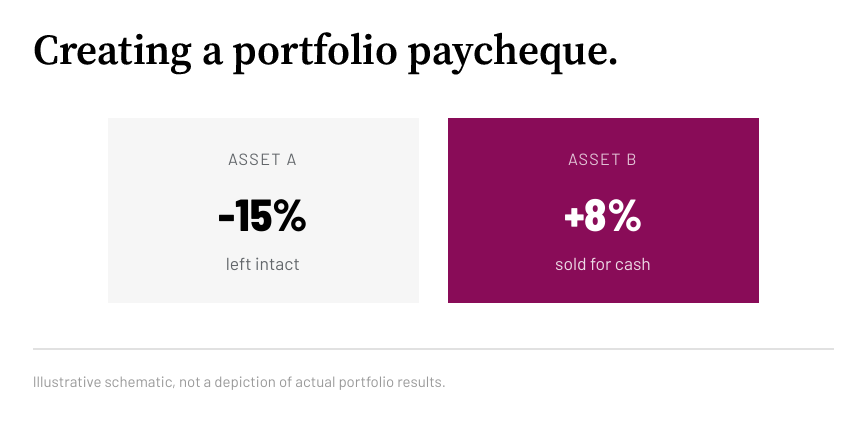

Creating a portfolio paycheque

Retirement income does not need to depend on whichever investments happen to pay the largest dividends.

A portfolio paycheque starts with the household’s actual spending requirement. Cash may come from available reserves or from investments that have appreciated and moved above their target weight. An investment that has recently declined may be left intact, provided it continues to serve its intended role. Taxes, account structure, and the broader financial plan are considered at each step.

This approach works alongside rebalancing. It can reduce the need to sell assets after a period of weakness, keep the portfolio aligned with its risk target, and adapt as markets and spending needs change.

Dividends follow a company’s payout schedule. A portfolio paycheque can be adjusted to the investor’s needs.

The takeaway

Your spending needs should determine your withdrawal plan. Dividend yield should not drive portfolio construction.

A total-return approach provides greater flexibility to diversify broadly, manage risk, and create a planned source of cash flow without requiring every investment to produce income in the same way.

Caldwell Group

Richardson Wealth Limited